In

this

piece Surjit Bhalla of Indian Express bashes monetary policy

and claims that he has found the panacea to kill inflation. The blurb of yesterday’s piece is that it is

the MSP, the stupid. If you want to control inflation either reduce it or

freeze it. And if you can’t then reduce interest rate. It will unleash the

animal spirit of the Indian entrepreneurs. Indian growth story, he claims, will

soon resume its pace. Much of Mr Bhalla’s claims are does not stand the

scrutiny.

He

begins his piece by saying that he is pleased to see CPI-inflation at 7.8%. Maybe,

it is comforting for a man like him who gets a six-digit pay check. But he does

not give this credit to RBI. He is of the view that RBI’s epic battle (by

hiking the repo rate) since March 2010 has done little to control inflation,

which is true. Both inflation and inflation expectation (a quarterly survey

conducted by RBI) is very high, much beyond RBI’s comfortable level. But Bhalla

gives credit to RBI’s clear communications: that it will keep repo rate high

till inflation cools down, the talk of inflation targeting, anchoring inflation

expectations. I will come back to this bit later.

Then

Mr Bhalla claims it is sheer nonsense to explain Indian inflation by using

stuffs like money supply, credit growth, and fiscal deficit. Econometrics

investigation, he argues, offers zero explanation of Indian inflation.

Then

one fine morning he invents a model that can solve age-old problem of inflation

in India. How was he able come with this earth-shattering idea? He found the

bad guy – minimum support price (MSP). He trusts his model so much that he

challenges (oh yeah, it’s a friendly challenge!) RBI and other inflation-concerned

people to prove him wrong. It succeeded intimidating me.

Unless

we see his research paper we can’t comment his model. Unfortunately,

downloading that paper was not possible. We don’t know if variables are

subjected to unit root test (to test whether they are stationary). My first gut

reaction after seeing his model how can one explain Indian Inflation – so

complex – by using only one independent variable? I thought two-variable model

exists in the intro econometrics textbooks to teach students in the classroom.

No, i was wrong. It seems Mr Bhalla has taken it seriously, so seriously that

he recommends his policy advice to GoI on the basis of his toy model.

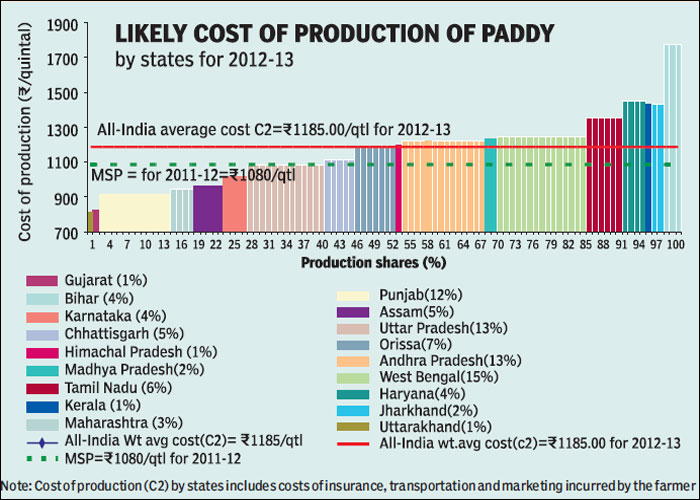

Okay,

let’s verify his claim that MSP is the stupid. He says MSP is rising because of political reasons. He can't be be ignorant of cost factors. MSP is rising because input cost

is

rising

(see Chat

7 of Rajan’s speech). Cost is rising because government is

setting administered prices free and rural

wage

(see Chat 8) driven by NREGA. Despite rising MSP, the terms of trade of output price to input price remains more or less same (See Rajan’s speech). fact, the MSP provided by the GoI is comparatively much

lower than what other countries provide.

{kind=link}

But

nobody downplays the role of MSP and the behind-scene politics. MSP growth is

correlated with inflation. If we want the right MSP, then CACP should be

empowered, given full autonomy and its recommendations must be mandatory.

Institutional reform is necessary for CACP, FCI.

But

saying that MSP is entirely behind the inflation is ridiculous. A simple way to verify his claim is to check what has happened to the price of non-MSP food

crops. In fact, Ashok Gulati, former chairman of CACP argues that prices of

non-MSP goods have risen more than MSP goods. If this is true, how logical is

to argue that it’s the MSP, the stupid?

In

his attempt to provide the earth-shattering model he loses sight of other

factors that are also largely responsible. In my view, the elephant in the room

is the distribution of foodgrains (see Kausik

Basu’s paper).

Now assume that his model is a fine. So what does he recommend? Surprisingly, he

did not say anything about MSP. You would expect him to recommend: either to

freeze MSP or reduce it. But he recommends cutting repo rate. Since it does not

stem from his model i guess it comes from his frustration to see RBI not paying

heed to the Indian Express columns! (Just kidding). I guess he recognised the

fact that is politically difficult to freeze MSP; so he did not say anything

about what to do with MSP.

I

have never seen anybody giving recommendations beyond what his model says. In

his model, interest rate does not exist. How can he claim that interest rate

does not matter for inflation? Further, if he believes that interest

rate is holding investment, then he should show it. He should run a model regressing

investment or growth on interest rate.

Now

think of freezing MSP and assume that it is politically possible. Given that farmers

are habituated to MSP growth every year they may react sharply by

reducing production which will be double whammy. How much production will

decline depends on the elasticity of production with respect to MSP. Freezing

is good idea. But in the short run production will fall as a result of freezing and

thus, price will rise. However, it is good in the long-run. So, this is not the

right time to freeze given that input cost is also rising due to freeing up of

administered prices.

Since

he is bashing monetary policy because of high interest rates, it makes sense to

ask: what is holding back the India Inc? High interest rate, stagnant global

economy, economic uncertainty (govt’s policy mess/lack of clarity), corruption

or agricultural

stagnation?

He

seems to believe that if we reduce interest rates then economy will bounce

back. But he forgets that repo rate hike affects only 0.5 per cent of the entire

borrowing of the banking system. Stated otherwise, it is not a constraint to credit supply and liquidity. This is a very important point which has been

missed in the debate and discussion on monetary policy since Governor Subbarao

was habituated with raising interest rates.

High

interest rates are not a major problem that the India Inc is facing, rather the

messy (now it is changing) domestic policy atmosphere that drags the India Inc.

Rajan and his predecessor has ensured that liquidity is not a problem. And i

also think that liquidity is not a problem. If Bhalla is very concerned about

falling GDP figures, then he should pray that Modi government rolls out the

much needed reforms almost in all sectors. I can bet that FDI and domestic

investment will flow like flood. High

interest rate sometimes lead to high investment.

Yes, you hear it right. Mr Raj Chetty - a Harvard Professor, who won last

year’s JBC medal – has shown it. His mentor Feldstein was convinced. Then why

is investment low in India? I think Baker, Bloom, and Davis provides us the clue. It’s not the interest

rate, the stupid, rather the economic uncertainty (foggy policy). A large

literature has spawned off following the works of Baker,

Bloom, and Davis (see India’s policy uncertainty index, it is very high as of

August 2014) showing how high policy uncertainty leads to reduction

in investment.

Sure,

Rajan can’t claim much credit for

falling of inflation figures. It may be sheer luck. But today’s monetary policy

(New Keynesian models) works on how well a central bankers communicates with

public, expectation management, commitment to any monetary policy rules. It may be Prime Minister Modi too. People

know Rajan means business. He talks tough on inflation and also he walks the

talk. But then media reports said that Rajan might lose his job if Mr Modi

comes to power. But this did not happen. Mr Modi reposed faith in Rajan. This

sends a clear, loud, very strong message to the market that both are serious to

kill inflation, the bad guy. This might have led public’s slowly-declining

inflation expectation.

It

raises question why RBI has so far not succeeded in bringing down inflation?

RBI’s baby step approach (hiking repo by 25 basis points) is criticised by

economists. That makes it always behind the curve. In my blog post i argued RBI

should have gone for big hikes in repo rate if it was serious as Mr

Subbarao lamented later.

So,

where should we go from here? The declining numbers may give cheer to central

bankers. But i think they can’t allow the situation go out of control. They

should not reduce interest rate; rather keep it high where it is now. If they

reduce it and if Inflation rises then both Mr Rajan and Mr Modi will lose

credibility. Public will view that the duo have accepted defeat against the

Inflation Goliath. This thinking has serious repercussion on future monetary

policy and its success. It will jeopardise their credibility, inflation

targeting will lose all its charm (i don’t endorse India to adopt inflation

targeting. The time is NOT ripe now. However, we may try with some loose form of IT).

People may lose faith in monetary policy.

More

importantly, we have enough research showing that when headline inflation stays

high for a lengthy period, it is highly dangerous for the economy for two

reasons. First, it will lead to permanently high inflation expectations. Second,

high headline inflation or food inflation is translated in to high non-food or

core inflation via high and sticky inflation expectation (see Walsh, Prachi Mishra).

Indian

inflation is so complex that any careful student of inflation would adopt a

balanced view: it is due to demand factors like money supply, fiscal deficit,

NREGA expenditure, shifting dietary pattern (due to rising rural

wage?);

and supply side issues like MSP, distribution of foodgrains, poor monsoon

(resulting agricultural falling output), international raw material prices,

global prices of oil products and foodgrains. And yes, exchange rate is also

important. He seems to discredit all those factors.

Since,

RBI has been fighting an epic battle it must win at any cost. It can’t let the

situation slip from its control at this time where victory seems visible. Let

us hope that RBI wins this epic battle as soon as possible.

Update

I found this IMF article by Rahul and Tulin which says heightened policy uncertainty and deteriorating business confidence have played a key role in the recent investment slowdown. This is basically what my blog post is arguing. (read here the blog post by the authors)

Update

I found this IMF article by Rahul and Tulin which says heightened policy uncertainty and deteriorating business confidence have played a key role in the recent investment slowdown. This is basically what my blog post is arguing. (read here the blog post by the authors)