The recent announcement by the RBI has surprised the market

participants. The RBI chooses to reduce the short-term repo and reverse repo by

50 basis points each. RBI has also duly acknowledged the upcoming upside risk to

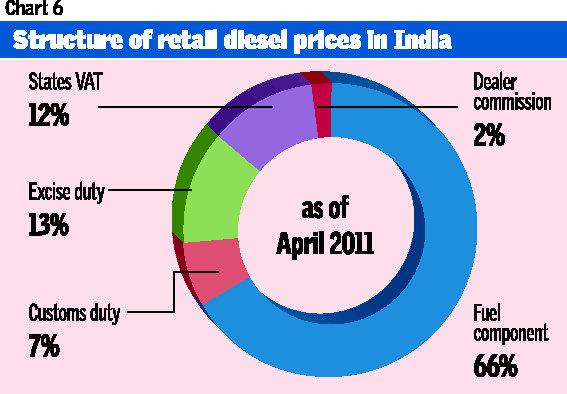

inflation. That the oil marketing companies demanding for higher prices of

petro-products day after the annual monetary policy is announced is a pointer

to it. It seems that RBI is more concerned about growth. In fact this is the

‘sacred mantra’ which every policy maker is chanting and mad for.

Recognising its failure to combat inflation and the single minded

growth objective has led the RBI to increase the threshold inflation to 6.5% in

the medium run. So the earlier tolerable inflation of 4.5% will be a history. While

most of the developing countries like Brazil (it embraced inflation targeting in 1999) and South Africa (2000),

and Ghana (2007) are chasing inflation, our central bank is ‘macho’ about growth. Note

that 6.1% growth rate (third

quarter of last fiscal) is not a bad figure at all. But

expected inflation of 6.5% is surely a bad music to ears of ‘mango people’. To

bail out United States from the protracted recession Harvard Economist Ken

Rogoff proposed higher inflation that got supported by his Harvard colleague

Greg

Mankiw, even from the current Fed Chairman Ben Bernanke, Christina

Romer, President Obama’s former Chair-woman and many market monetarists and

Nobel laureate Paul

Krugman. Despite the severity of recession yet the Fed has not pursued this

policy. It clearly demonstrates how much significance they offer to inflation

(Note that US inflation rate is even below The Fed’s unofficial target of 2%).

RBI’s rate cut of this magnitude may be based on five reasons.

First, an unexpected bigger cut would provide commercial banks enough incentive

to lower its lending rates. Second, the transmission mechanism will be more

effective and take less time. Third, the RBI tries to learn from its past

mistake. One reason why the increase in policy rates could not help much in

reducing inflation in a timely manner is that the ‘baby-step’ or the

‘piece-meal’ approach of the central bank. Hence, it thought that so as to have

a bigger impact on the outcome it needs to cut drastically the policy rates.

Fourth, by lowering rates, the RBI sent signal to the foreign investors that

cost of doing business has lowered. And finally, the RBI wants to infuse more

liquidity to the market.

But the very first reason may not be achieved. It is because while

higher policy rate motivates the commercial bank to increase the interest rate,

this may not be the case when the RBI lowers its key policy rates. The reason is

that commercial banks are now vying to attract savers through increased deposit

rates. Further, RBI has also

increased the flow of the saving deposit rates. Another factor that might pour

water in the hopes of the Governor Subbarao is the “uncertainty” factor. Banks

are not sure whether there will be any further rate cuts. In that case banks

are expected to maintain status quo, limiting the effectiveness in the

transmission mechanism unless they are being pressed by the finance ministry.

Rationale

It is not difficult to nail down the motive behind the cut in policy

rates. RBI cited in its monetary policy statement that the deceleration in the

economic growth is the result of slower industrial growth. Further, RBI should

not panic at the falling Index of Industrial Production (IIP) which is highly

fluctuating and are far from credible and calls for scrutiny. Again, RBI thinks

that liquidity was squeezed as credit demand both from industry and agriculture

has not peaked up. This leads to contraction in gross fixed capital formation (GFCF)

both in the second and third quarters of last year. In other words, the RBI

thinks that money was tight for this period. Though private GFCF are below the trend

since 2008-09, but they have rebounded following a drastic fall in 2008-09. Hence,

quarterly fluctuations do not warrant such steep cut on the policy rates given

that both WPI inflation and CPI inflation are hovering around 7% and 9%

respectively. Since the onset of high interest rates, the growth rate of credit

to industry remains stable. Agriculture recorded a steep fall in the credit

growth from 22.9% in 2009-10 to 10.6% in 2010-11.Two factors contribute to

this. First, the impact of high interest rates and second, the non-food credit

growth rate has increased from 16.8% from 2009-10 to 20.6% in 2010-11. The behaviour

of eight core industries shows that the growth rate is around its trend rate of

5.5%. Though these falling numbers call for a reduction in the policy rates we

need to ask as to who contributes more to it: global slowdown, higher interest

rates, or supply side problems? It seems that the current understanding of the

RBI is that our growth has slowed down because of global slowdown which is not

entirely right. Growth has been robust following the sharp decline in 2008-09.

Rather, the major contributor to the economic slowdown is the almost zero

growth rate of agriculture. Agriculture is still the major determinant of

growth and inflation. Agricultural performance feeds through to the rest of the

economy through supply and demand linkages. Reduced agricultural growth reduces

supply to industry, thereby reducing industrial production. Further, a reduced

income from agriculture and the fact that they spend more on the food stuffs

also contribute to the contraction in demand for industrial production. Hence,

the decline in industrial performance is not that investment is not picking up.

Rather, the diagnosis and the solution remain elsewhere.

The best option could have been to let the policy rates remain

intact and wait till the next mid-quarter review to see the evolution of both

WPI and CPI inflation and how GDP and IIP behave. The RBI’s policy moves will

not help much. Instead targeting inflation could help better achieve more

economic growth. A 2011 article in the prestigious Journal of Policy Modeling, written by Salem Abo-Zaid and Didem Tuzemen has shown that the effects of targeting inflation

in developing countries are associated with lower and more stable inflation, as

well as higher and more stable GDP growth. They also conclude that

non-targeting countries would highly benefit from targeting inflation. In the

least case will may have higher GDP

growth (satisfying needs of the policy makers and of the government) and higher

inflation (surely, welfare-reducing to ‘aam aadmi’. If any central bank, facing a declining

industrial production and hence, economic growth and high inflation, they must

ask this question before advancing for monetary policy: how much of the benefit

a poor man extracts if it increases the growth rate by one percentage point

more compared to how much of the benefit a poor man loses if it increases the

inflation rate by one percentage point more (or if there is a chance that

inflation might increase) or it does not any take any step to reduce inflation

from high rate.

Solution lies elsewhere

While much of the solution lies in the government, it tries to save its image through the

rise in GDP. Hence, the government

thinks that high interest rate has stifled down the growth rate of GDP. So the pressure from the government cannot be

ruled out in easing the key policy rates. By reducing the policy rates, the RBI has put the ball in the government’s

court. First, to address its fiscal deficit,

it needs to reduce subsidies. If it does, it will increase the petro prices and urea prices. It will be

translated in to higher headline inflation. And if it does not, it may result in

the crowding out of private investment (examining the crowding out hypothesis for

India for the period 1970-71 to 2009-10, Jagadish Prasad Sahu and Sitakanta

Panda in a 2012 article in the prestigious Economics Bulletin have

empirically shown that government investment crowds out private investment in

the long run). Only the 2G/4G auction and embracing the GST can help the government

in correcting the fisc. Government must address the supply side issues promptly

and boost the agriculture investment and reducing the subsidies which will help

in the long run. It must cure policy paralysis, remove the infrastructure

constraints; raise the ease of doing business, and lessen the time overruns. It

must recognise the limits of the monetary policy which can’t control these

factors.

In the pursuit of growth RBI

should not heap misery on more than half of the country’s population. We can at

best wish for the victory of RBI’s great gambling and optimism.